Capex

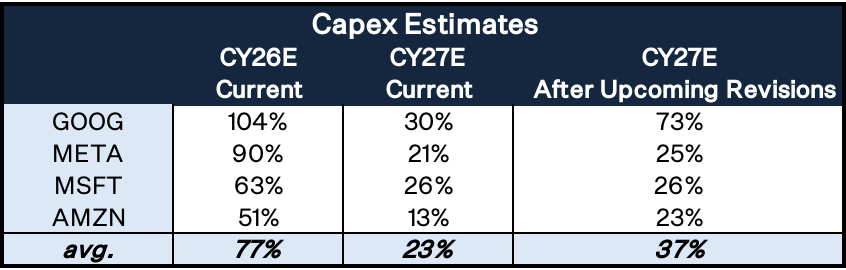

Within the hyperscaler capex conversation, the key metric is next year’s growth. As it stands, the Street is looking for 23% growth in CY27. That said, whisper expectations have moved higher following Google’s $85B and Amazon’s $25B capital raises, which will be spent predominantly late this year and into next year.

For the sake of simple math, if you assume $80B of Google’s $85B raise goes to next year’s capex and $20B of Amazon’s $25B raise goes to capex, hyperscaler CY27 capex growth lands at 37% y/y. Additionally, I expect a modest increase in Meta’s CY27 capex outlook, which should push its growth to 25% from the current expectation of 21%. The biggest narrative risk in the capex conversation is Microsoft, where I believe management will guide investors to an unchanged 26% growth rate for next year. If three of the four hyperscalers raise their outlook, I believe the AI infrastructure narrative will remain intact. The buildup is outlined below: