The Air

Back on September 9, when the new iPhones were launched, I wrote that what matters most is form factor and Apple successfully landed two winners, the Air and the new Pro models. Turns out, I was wrong on the Air. Third party survey data and supply chain reports suggest the Air accounts for around 5% of total unit sales.

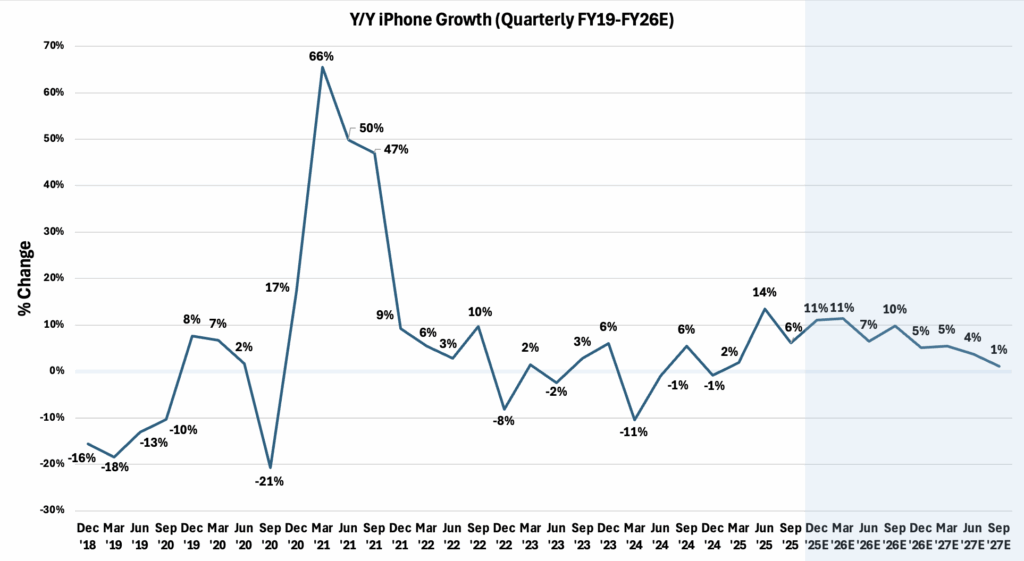

The reason I missed it was that historically a new form factor matters. Looking back, iPhone sales have seen a bump following meaningful changes in design. This year we got two, the Pro and the Air. Together, I thought in September these models should account for about 70% of iPhone revenue, with 55% being the Pro.

Despite Apple positioning the Air as a Pro level device, it has noticeable gaps in camera features and battery life. Yes, its aesthetics are impressive, but the functionality still lags the Pro line.

What matters most is that both the Air and Pro introduced eye catching new hardware designs. New hardware designs have typically boosted revenue growth. When the iPhone 6 and 6 Plus launched in 2014 with larger 4.7 inch and 5.5 inch displays compared to the iPhone 5’s 4 inch display, it powered a super cycle. iPhone revenue in FY14, the iPhone 5 cycle, grew 12% y/y. The 6 and 6 Plus drove revenue up 52% in FY15.