Strong Fundamentals, Tired AI Trade

There was a lot of good news this week, yet the AI trade shrugged it off. TSMC and ASML both guided September revenue higher than the Street. IBM’s poor results (down 26% this week) were actually a positive read on how early we are in AI, showing a new dynamic in AI infrastructure spending: it’s so powerful that it is pulling dollars away from IBM’s traditional hardware and software businesses. Separately, AAPL shares received a boost, up 20% over the past three weeks vs. the Nasdaq up 1%, on early signs that the new Siri, which marks the start of personalized AI beta, finally shows that the company has chops in AI.

All that said, with the exception of Apple, the market did not reward all the good news.

The Innovator Deepwater Frontier Tech ETF (LOUP), which has a thematic AI weight of 70%, was down 6% this week, TSM was down 9%, and ASML was up 1%, compared with the Nasdaq, which was down 2%. The exception was Apple, up 4%. The reason for the disappointing stock reaction: the trend that emerged in April continues. Beats and raises are no longer enough to move AI stocks higher. The question is what will change the tide.

TSM:

TSM’s June revenue was already reported earlier in the month, so the earnings report was all about the guide. September guidance implies 42% y/y growth versus the Street’s 36% expectation. Full year 2026 guidance moved from 37% to the low 40s, and the math behind that raise implies the December quarter accelerates from the 42% consensus to growth of 50% or more.

The negative is that margins are topping out. The recently reported 68% gross margin compares with the September quarter margin guidance of 66% (midpoint), which suggests the first margin decline since June 2025 and the first decline of 1% or more since December 2023. In other words, for the past year, margins have been moving higher. Now they’re moving lower. My sense is that they will actually print 67% margins in September, given the favorable pricing environment, which would be positive compared with current expectations calling for 66%.

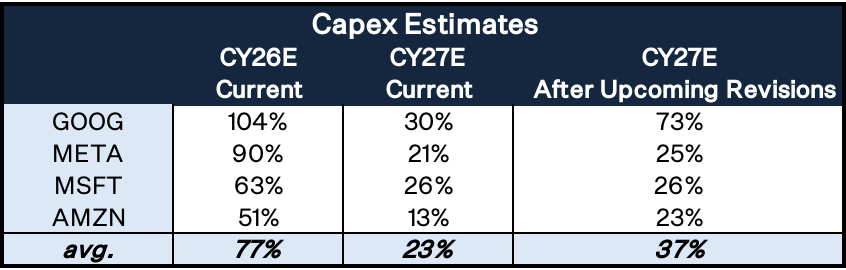

The company also raised capex for CY26 by 15%, which means it’s now expected to grow this year by 59%. Some investors read that as a negative because it points to endless spending. We see it as a positive, given that increased TSM production capacity, especially in the US, makes it next to impossible for a competitor to gain share. Management also guided for capex to be up “significantly” over the next few years. While the word “significantly” lacks the detail that would be helpful to model the spend, the Street’s current estimates, calling for capex growth in CY26 of 59%, CY27 of 23%, and CY28 of 18%, imply that total capex in the years CY23 to CY25 will double compared with CY26 to CY28. That, in my estimate and the Street’s, feels in line with “significantly.” I’m not expecting a bombshell update to capex that will change Street estimates when the company reports in September. I do expect the capex growth numbers to inch higher. In other words, the steepest part of the curve is behind us.

IBM:

IBM was an early indicator of legacy software budgets being redirected to fund AI development. Software, at 45% of revenue, grew 11% in the March quarter, was expected to grow 10% in June, and grew 5%. In the world of IBM results, which have been steady over the past 20 years, that small miss was actually massive. Shares of IBM traded down 25% the following day, marking their worst day of trading. That miss tells us two things: the desire among Fortune 500 companies to build AI infrastructure is growing, and the risk that traditional software will be displaced is also growing. At its core, software provides humans with an abstraction layer that allows them to interact with the machine. Bots or agents don’t need the layer; they just talk to each other. Large enterprises are actively sacrificing core, historic products to build out their AI future.

ASML:

Despite a naturally lumpy business driven by machines that sell for $250M to $400M each, ASML grew June quarter revenue by 21% versus expectations of 16%, an acceleration from 13% growth in March. September guidance implies 60% y/y growth versus the Street’s 51% expectation. Full year 2026 guidance moved from 22% to 38% y/y, and the math behind that raise implies the December quarter accelerates from the 40% consensus to growth of 54%.

The stock still fell 1% following comments in the earnings call that ASML expects to build around 85 EUV machines in 2027, below analyst expectations of 90 to 95. But ASML didn’t say demand is fixed at 95 units they can’t meet. CFO Roger Dassen said 85 reflects ‘the balance between demand and supply as we see it today,’ and that if customers ask for considerably more, ASML would revisit the supply chain to see what else can be done, just as they’ve done in recent quarters. So 85 is management’s current best estimate, not a hard ceiling. The big picture still holds: even a cautious, supply-balanced number like 85 points to continued strong growth at the company that makes the machines that make the chips, suggesting the hardware buildout is still in its early stages.

Apple:

This week, the iOS 27 beta, released in the US and featuring the newly overhauled Siri, is the first example of personalized AI that is a must have, and I believe it will drive a rerating of AAPL shares. I’ve been using it for the past three days, and while I find that the new Siri is slow and takes extra juice, the personalized insights between messages and mail are more powerful than I expected. I feel it’s an unlock in terms of the utility of the phone. This all matters because it finally reveals to investors, who have been waiting two years (since WWDC 24) for Apple to show that it has some AI muscle, that this muscle can be applied to Apple’s pursuit of a unique opportunity in personalized AI. I expect Apple’s progress with personalized AI will start a multiyear hardware upgrade cycle inspired by AI from CY27 through CY30. Shares of AAPL rallied on the news and finished the week up 4% vs. the Nasdaq, which was down 2%.