The September Spike

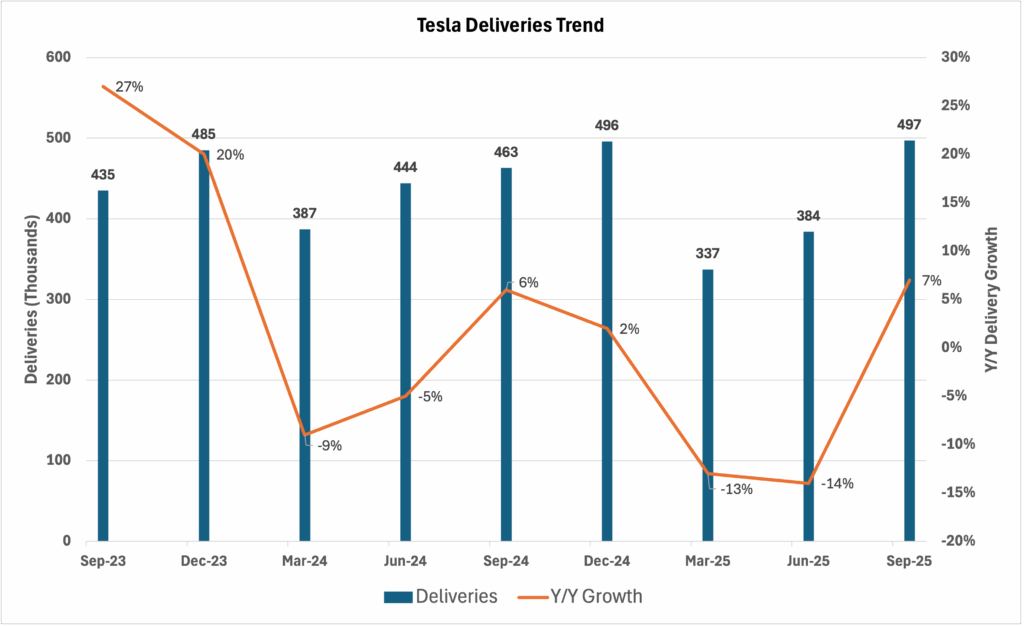

Deliveries of 497k raced past a 470–475k whisper range. The sell side had been raising numbers throughout the month of September, starting at around 440k, due to a combination of the success of the tax credit pull-forward and improvements in China.

I believe the China business did improve, and absent the tax credit would have yielded a meaningful improvement in deliveries to down 5% y/y compared to down 13.5% in June and 13% in March.

Tesla deliveries and growth rate:

By my estimation, the tax credit added about 55k incremental deliveries, a massive number in the context that in the June quarter I estimate they sold just over 150k cars in the U.S. That means the credit sunset caused the U.S. business to spike around 35% quarter over quarter.

While that number is eye-popping, it’s reasonable given the context that prices of Teslas would increase an average of 15% following the end of the credit. Elon has talked about the price elasticity of demand in the past, and has used that view as justification to roll out a more affordable model next year. This makes me believe that a looming 15% increase in price could trigger a 35% increase in demand.

This begs the question: if the strength in September was one-time in nature, why are shares trading only down 1% on the print, after being up 38% over the past month? A true “buy the rumor, sell the news” reaction would have seen shares down 5% or more on the delivery number.