Lead Times

There’s a debate about the value of tracking lead times. After all, we don’t know how much supply there is, which makes it difficult to translate lead times into a measure of demand. That said, my observation over the past decade is that longer waits typically line up with stronger cycles.

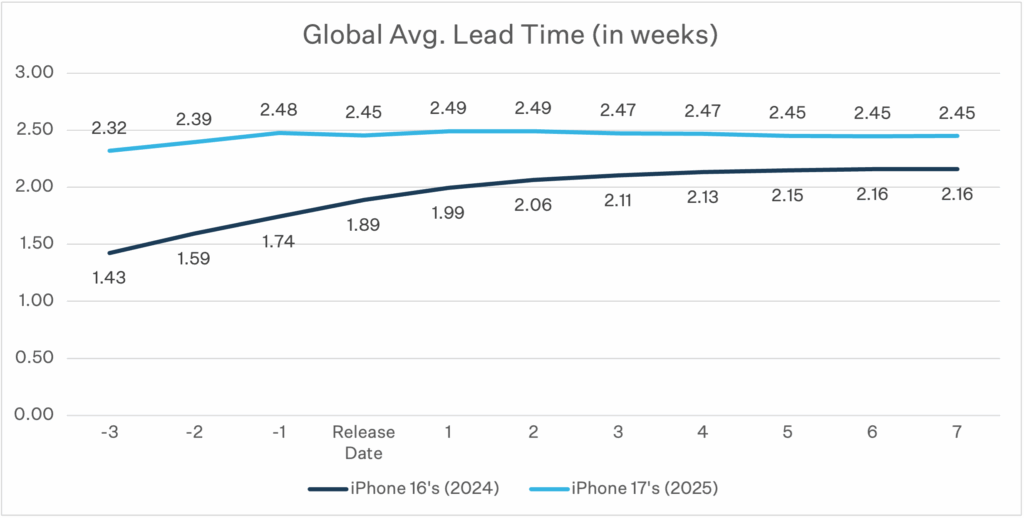

The global snapshot compares favorably with last year. Three days ahead of launch, iPhone 17 average lead times were 2.32 weeks, while iPhone 16 tracked at 1.43 weeks in the same window. From release day to seven days after, iPhone 17 lead times inched up to 2.45 weeks, compared to iPhone 16 at 2.16 weeks. The bottom line is lead times this year are about 10% longer than last year.

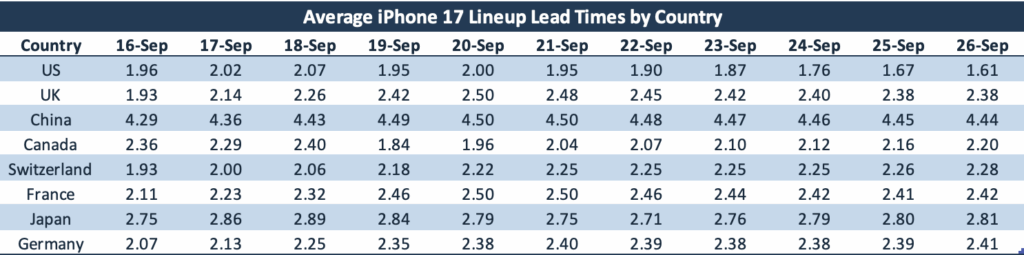

One dynamic that stood out in the country-level readings was that most countries were at around 2.5 weeks, while China was at 4.5 weeks. I don’t have a good explanation for the gap, especially since most of the phones are assembled in China.

Where are lead times going from here? There will be some noise in the numbers if reports are accurate that Apple has asked suppliers to boost production of the entry level iPhone 17 by about 30–40%. If base-model output increases as reported, aggregate availability will improve and lead times should come down in the weeks ahead.