Early Demand Signs

I’ve studied lead times for the past 15 years and have concluded that while it’s part art, part science, and longer lead times typically are a leading indicator of higher demand.

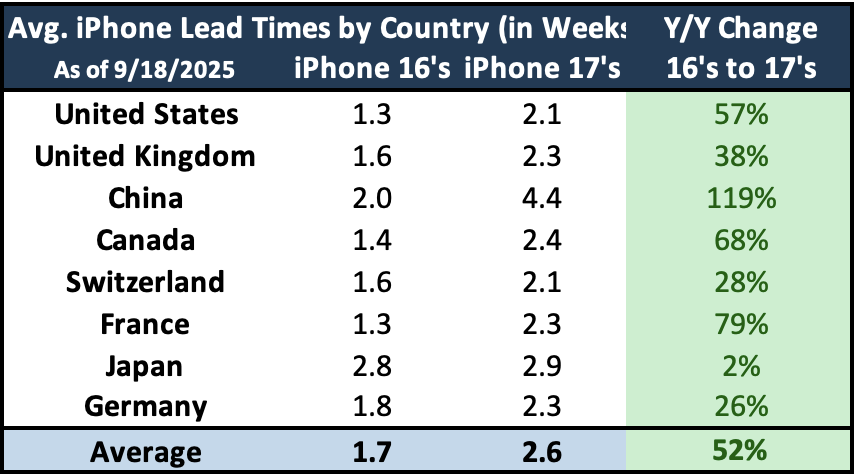

At Deepwater, we measured lead times for the iPhone 17 family on Apple’s online store in eight countries and found them currently sitting at an average delivery date of roughly 2.6 weeks, compared to about 1.7 weeks at the same point for last year’s launch.

The high-end Pro Max model is the longest wait at around 3.3 weeks, with the Pro and standard models closer to 2.3 weeks. What has surprised me the most is the new ultra-thin iPhone Air is readily available in most regions (often available for same-day pickup). While some may read this as a sign of soft demand, my view is that initial supply was greater than normal. That take is based on the fact that new form factors have historically been in high demand. It’s been 11 years (iPhone 6 Plus) since there has been as significant of a hardware change, which further suggests the lead times are impacted by greater supply.

China, which accounts for just over 15% of sales, stands out with an average 4.4 weeks for all models except the Air. The iPhone Air’s China debut is on hold due to a near-term regulatory delay: its eSIM-only design requires approval from Chinese authorities, so the Air is temporarily unavailable there.

Despite the Air’s absence, early signs suggest demand in China is strong. JD.com, a leading Chinese online retailer, reported that first-day iPhone 17 pre-orders exceeded last year’s iPhone 16 launch, and that excludes the Air.