December Deliveries

We expect December quarter deliveries to be down 16% y/y, below the Street’s estimate of down 10%. This puts December deliveries at 415k, compared to the Street at 449k.

Our estimate is below the Street because we believe growth in the business was similar from September to December after adjusting for the impact of the tax credit sunset in September.

Taking a step back, we believe September deliveries pulled forward 55k units that would have otherwise landed in December or March. For simplicity, we assume all of the pull forward came from the December quarter. That implies growth in September would have been down 5% if not for the 55k impact, a Deepwater estimate, from the ending of the credit.

For December deliveries to be down 5% would imply overall deliveries of 470k. Subtracting the 55k deliveries that landed in the September quarter gets us to 415k in December.

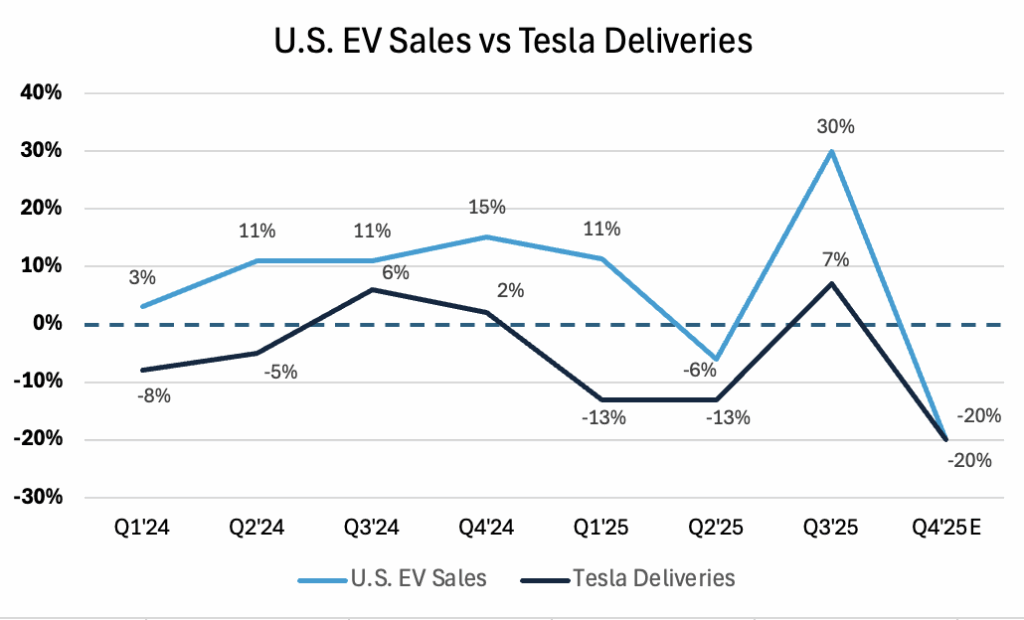

The table below outlines actual deliveries and the corresponding growth rates, along with deliveries adjusted for the impact of the ending of the tax credit.

From a market share perspective, if Tesla units are down 16% year over year in December, that would imply market share gains, given Cox Automotive is anticipating overall US EV sales will be down 30% year over year in December due to demand pull forward and a slowing overall new car market.